The innermost circle of the financial crisis

“Too central to fail” instead of “too big to fail”: whether banks pose a risk to the financial system when they get into distress has more to do with their level of networking than with their size. Economic researchers at ETH Zurich have developed a method to deduce the “systemic importance” of banks from their complex connections within financial networks.

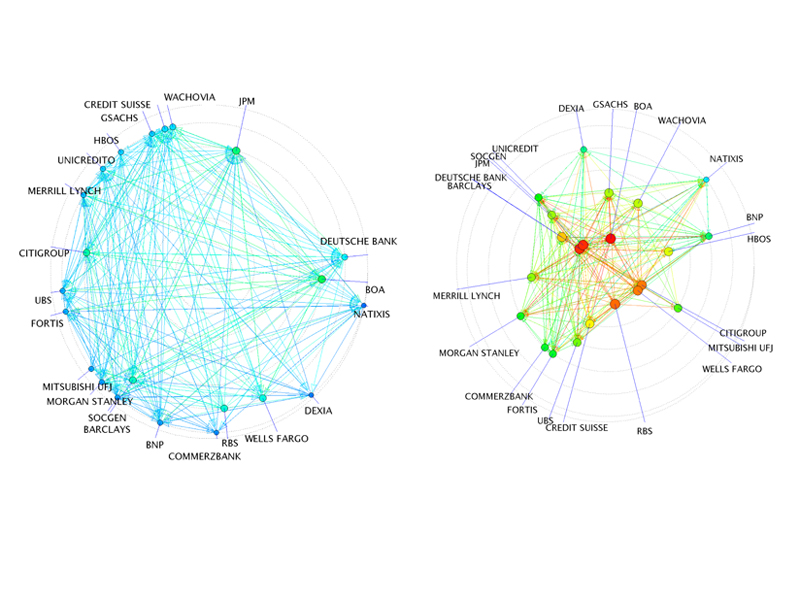

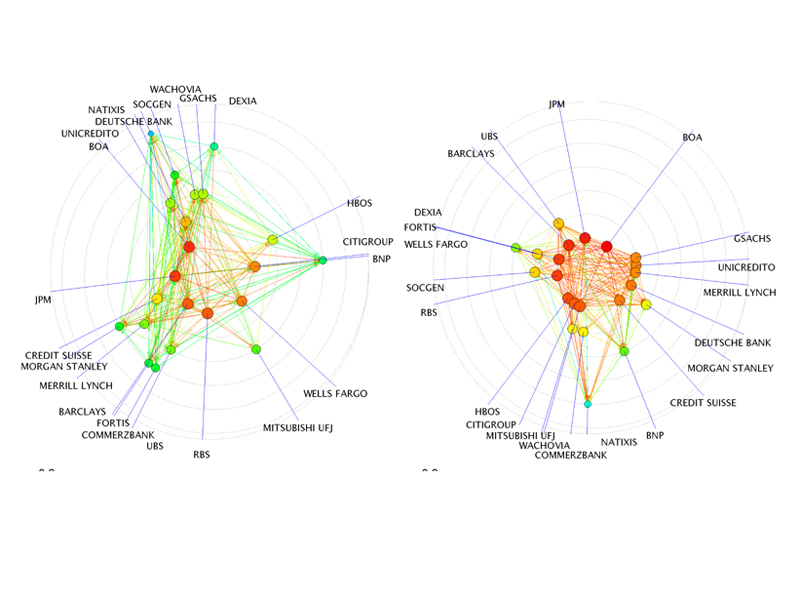

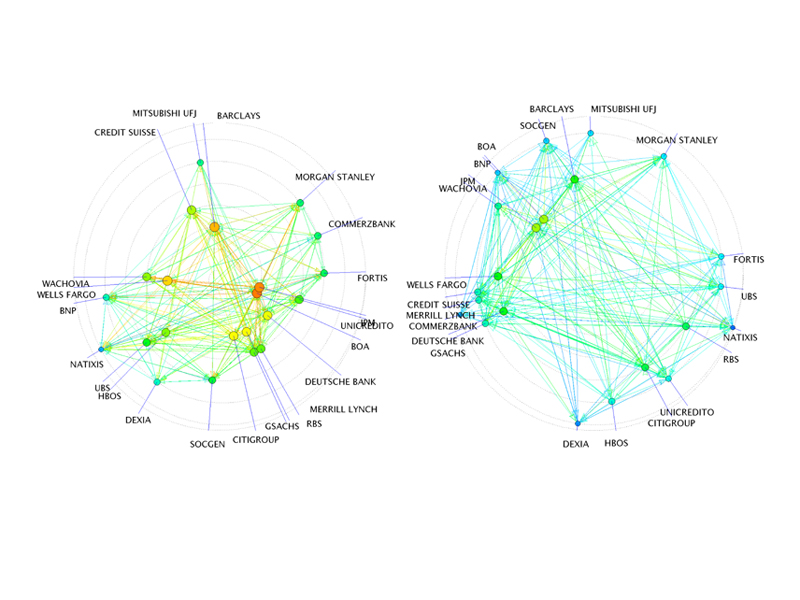

Between 2008 and 2010 a total of 22 banks formed the innermost circle of the financial crisis. They were so intensely connected with each other through credit relationships, mutual equity investments and financial dependencies that the distress of any single one of them could endanger the entire financial system. In November 2008, the emergency loans granted to these banks by the American Federal Reserve to protect the American financial system from collapse amounted to a total of USD 804 billion.

The interdependencies among these 22 banks were likely so strong that a small shock to the system as whole could get amplified into a systemic default. Thus the US Federal Reserve could not have allowed them to fail without creating serious consequences for the economy.

This is the conclusion reached by four economics researchers at ETH Zurich in a study published on 2 August 2012 by the online and open access journal Scientific Reports. This is a primary research publication from the publishers of Nature.

A fresh impetus

The paper by the ETH Zurich researchers injects fresh impetus into the debate regarding the systemic importance of banks that are “too big to fail”. A bank becomes systemically important, or “too big to fail”, when its services are irreplaceable and its insolvency would cost the national economy more than its rescue by the state. However, a bank’s size is only one indicator of its importance for the financial system.

Even small banks can pose systemic risks if they are closely networked with other financial institutions. However, the identification of such networking risks and interdependent credit risks presents major challenges for science, business and the authorities concerned. For this reason, the European Commission has launched the scientific project “Forecasting Financial Crisis (FOC)”. FOC is financed by the FET OPEN Scheme (“Future and Emerging Technologies Open Scheme”). Its research topic is to understand and possibly forecast systemic risk and global financial instabilities.

The

FOC-funded “too central to fail” approach developed by Stefano Battiston,

Michelangelo Puliga, Rahul Kaushik and Paolo Tasca at the ETH Zurich Chair of Systems Design, together with Guido

Caldarelli of IMT Lucca (Italy), is also pointing in this direction. Their

strategy is doubly innovative: on the one hand, it is based on original data

from the Federal Reserve, while on the other hand, the ETH Zurich researchers are

analysing the Fed data using a newly-developed network research method for the

first time.

Furthermore, the Swiss National Science Foundation (SNSF) is funding another project of this Chair on non-regulated over-the-counter (OTC) markets and systemic risk in financial networks. The results of the methodology can be seen interactively at http://ethz.focproject.net:8080/widget.

Emergency loans used as a data source

The Federal

Reserve data originate from the “emergency loan program” from 2007 to 2010, through

which the Fed provided “cheap” money to financial institutions in the USA that

were acutely at risk of defaults. At the height of the crisis, the total amount

of loans granted climbed to an astonishing USD 1.2 trillion.

The Federal Reserve published the figures after the US Supreme Court granted the Bloomberg business and financial information and news company the right to inspect the data, since the American financial system had, after all, been restructured using public funds.

The data sets from the Federal Reserve and Bloomberg document the residual outstanding debts and the market capitalisation of a total of 407 financial institutions that borrowed emergency loans from the Fed. The size of the loans provides an indication of a bank’s individual debt over equity ratio and of any potential distress or defaults.

The assessment of the Federal Reserve data showed that, although the various banks got into difficulties at different times, around 30 banks reached the peak of their emergency situation simultaneously at the height of the crisis. Considered over the entire duration of the emergency loan program, it also became apparent that the number of top borrowers at any given moment hovered around a figure of 20.

The ETH Zurich researchers then turned their focus towards those 22 institutions that had received more than USD 5 billion in emergency loans on average over the entire crisis period. This circle of top borrowers from the Federal Reserve also included the US-based branches of the two major Swiss banks UBS and Credit Suisse, which had averaged outstanding debts to the Fed amounting to USD 13.89 billion (UBS) and USD 13.29 billion (CS) between 2008 and 2010. This put them in 6th and 7th position among the top borrowers.

Google principle used to examine Federal Reserve data

The main

new feature in the ETH Zurich economists’ approach is their methodology: to discover

how the distress of a tightly networked financial institution impacts on other

banks and spreads through the network, they combined the finance notion of

balance-sheet contagion with methods from network science, including the

principle behind the well-known “PageRank” algorithm. This algorithm is at the

heart of the Internet search engine “Google”. The score of a webpage depends,

recursively, on how many other important

webpages point to that webpage.

In a similar way, in the “DebtRank”, introduced by the ETH Zurich researchers, the systemic importance of an institution is higher if its distress affects other systemically important institutions. This recursivity can be solved mathematically yielding a number measuring the fraction of the total economic value in the network that is potentially affected by the distress or the default of an institution.

“Many economists regard today financial systems as complex networks, in which the financial institutions constitute the nodes and the links between the nodes represent the banks’ financial dependencies,” explains Stefano Battiston. The researchers also drew on earlier papers by the Chair of Systems Design, which examined the global network of corporate control.

The study enables them to estimate how central a bank’s position is within the financial system, and what risk it poses. In this sense, “DebtRank” serves as an indicator of a bank’s level of networking and thus its systemic importance.

Further Readings

Battiston S, Puliga M,

Kaushik R, Tasca P, Caldarelli G (2012). DebtRank: Too Central

to Fail? Financial Networks, the FED and Systemic Risk. Scientific Reports, published online

2 August 2012. doi: 10.1038/srep00541.

Battiston S, Delli Gatti D, Gallegati M,

Greenwald B, Stiglitz JE (2012). Liaisons dangereuses: Increasing connectivity, risk sharing, and

systemic risk, Journal of Economic Dynamics and Control, 36 (8): pp. 1121-1141,

doi: 10.1016/j.jedc.2012.04.001.

Battiston S, Delli Gatti D, Gallegati M,

Greenwald B, Stiglitz JE (2012). Default

cascades: When does risk diversification increase stability?, Journal of

Financial Stability, 8 (3): pp. 138-149, doi: 10.1016/j.jfs.2012.01.002.

Vitali S, Glattfelder

JB, Battiston S (2011). The Network of Global Corporate Control. PLoS ONE

6(10): e25995. doi:10.1371/journal.pone.0025995.

READER COMMENTS